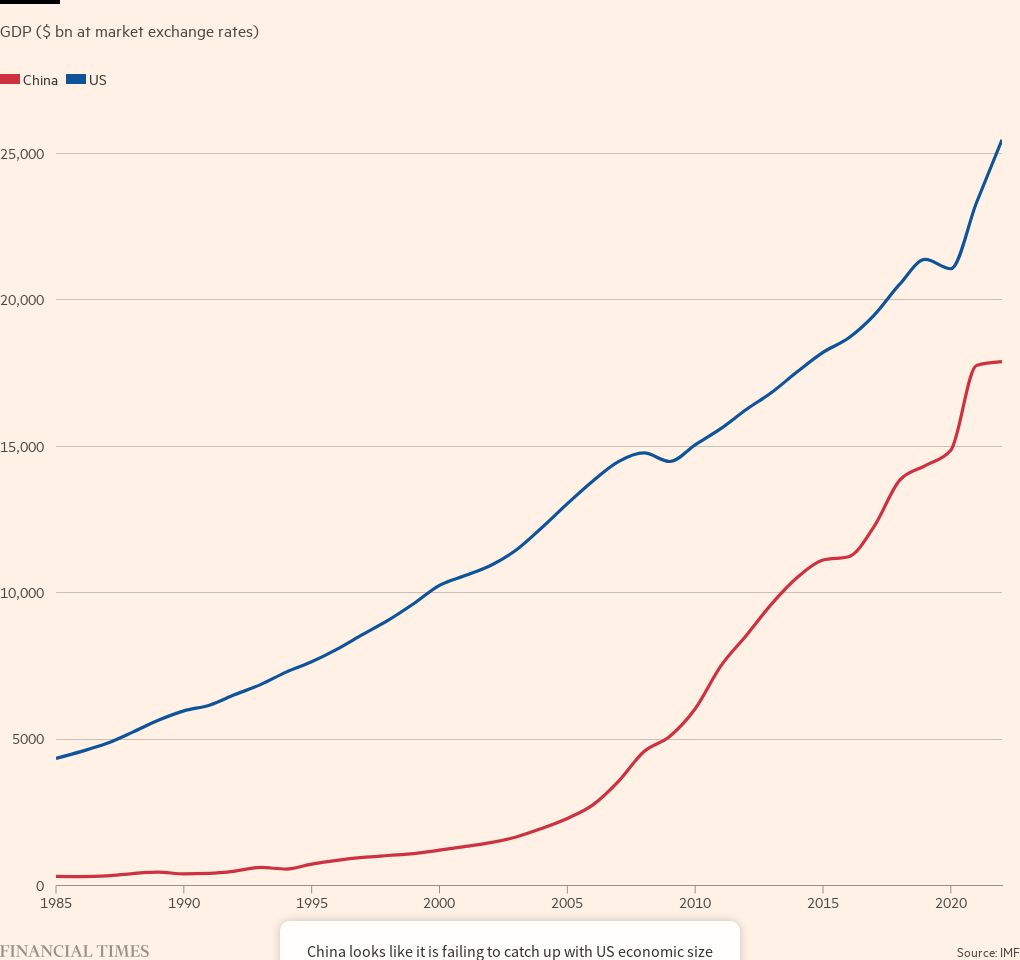

Evaluating Xi Jinping’s Industrial Strategy: Will it Revitalize China’s Economy?

The best Roth IRA accounts are usually free to set up and offer multiple investment types. Our list includes SoFi, Fidelity, Charles Schwab, and more.

The best Roth IRA accounts are usually free to set up and offer multiple investment types. Our list includes SoFi, Fidelity, Charles Schwab, and more.

Measures that show the opposite have absurd implications and dangerous policy prescriptions

Share prices are surging. Investors are delighted—but also nervous

Canada’s economy rebounded in the fourth quarter from a mid-year slump. Read more on the GDP data

Today, we got a sense of how consumers are feeling about the economy and it wasn’t as confident as previously thought.

Until the Bank of Canada starts cutting, higher interest rates promise more pain to come for Canada’s economy. Read on

Canada’s inflation rate decelerated to 2.9%, possibly opening a window for the Bank of Canada to start cutting rates in June. Read on

A North Carolina teacher has found a unique way to encourage her students to attend class and get them excited to learn.

Experts say a slowdown is coming, but a recession remains unlikely.

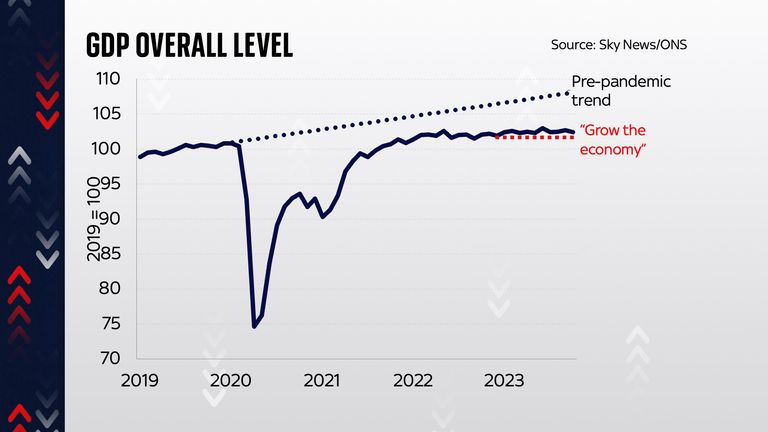

An average worker in the UK has lost £10,700 poorer annually due to wage stagnation, according to a report titled Ending Stagnation – a New Economic Strategy for Britain.

Navigating Through Uncertain Economic Waters The resilience of the U.S. economy defied expectations throughout 2023, fueled by robust consumer spending and substantial job growth, despite …

China may be the world’s biggest buyer of iron ore, but even that powerful position doesn’t mean that Beijing can succeed in dictating prices for the…

Overview of Economic Conditions in 2023 The year 2023 marked a period of economic stabilization following the tumultuous events of 2022, characterized by less volatility …

Canadian consumers were clobbered by skyrocketing interest rates and stubbornly high price growth last year. They should see progress on both fronts in 2024. But the new year will also bring new challenges.

Canada’s inflation rate was unchanged last month, holding steady at 3.1 per cent, above the Bank of Canada’s target range. Find out more

As Americans and the markets ready to enter the new year, financial author Harry Dent warns 2024 will bring the “everything bubble” to a burst “of a lifetime.”

P&G India, NetApp, MG Motor and Dell Technologies are among organisations enhancing their employee wellbeing offerings to include financial wellness and awareness. With a predominantly young workforce that is looking to understand not just personal finances better but also invest effectively for maximum returns, the focus is on driving knowledge around mutual funds, shares, derivatives, as well as government-provided investment plans, industry insiders said.

Into the final weeks of 2023, more inflation data will keep the markets occupied with CPI numbers out of the UK, Eurozone, Japan and Canada while the US updates core PCE data.

A populist surge is partly an understandable response to rising within-country inequality and reduced social mobility.

The market prognosticator said the predictions for 2023 were among his ‘worst years,’ after a widely predicted recession did not materialize.

Rolling coverage of the latest economic and financial news

Pradhan Mantri Jan-Dhan Yojana is an important and strong pillar in ensuring financial literacy of the country, former Union Minister Suresh Prabhu said, emphasising that it is very important to ensure practical financial security as it has a broader societal impact.

He was speaking at a

Across the country, community-based solidarity economies are emerging. While many are still nascent, they portend the possibility of larger-order transformation.

After being too pessimistic this year, analysts’ forecasts for 2024 have have swung too far in the opposite direction.

According to the World Bank, Bangladesh has been one of the fastest-growing economies in South Asia in recent decades, with an average Gross Domestic Product (GDP) per capita growth of above 5 per cent in the last decade. Moreover, the per capita income has also been steadily increasing and now exceeds neighbouring India’s. Such impressive economic growth has been accompanied by the increased number of vehicles on the roads. With economic prosperity and activities, the movement of people has increased manifold, and to facilitate their movements, there has been an uptick in the number of transport services and investment in road infrastructures. This article will discuss the impact on road vehicles due to economic developments in Bangladesh by running a Kuznets Curve Analysis.As of June 2020, the number of road vehicles registered under the Bangladesh Road Transport Authority (BRTA) stood at 4,471,625. According to the Bangladesh Bureau of Statistics, the average growth was 7.5 per cent from 2010 to 2020, encompassing all types of vehicles, from bikes to buses. A correlation exists between the increase in vehicles and the country’s per capita income, as the per capita income has also been rising with a year-on-year rate of 9 per cent in the fiscal year of 2021-2022, at US$ 2824. While buses and ‘auto tempoes’ (three-wheelers) are the key means of public transportation, micro buses, private passenger cars, motorcycles, and taxi cabs are considered private transports. Under this consideration, the number of public road transport vehicles is 101,687, and that of privately owned road transport vehicles 476,415, according to BRTA. TRANSPORT KUZNETS CURVE: Kuznets curve expresses a hypothesised relation among industrialised nations experiencing a rise and subsequent decline in income inequality. American economist and Nobel laureate Simon Kuznets first proposed the Kuznets curve in the middle of the 1950s. The relationship between inequality and per capita income in an economy is represented by an ‘inverted U’ in the Kuznet curve. In other words, growth in a weak economy would inevitably lead to greater income inequality. To establish a Kuznets curve analysis for public transport, the number of public vehicles from 2011 to 2019 is on the horizontal axis, and data on per capita income is on the vertical axis for the same period. In addition, the same is true for the one analysing private transports by taking the number of privately owned vehicles from 2011 to 2019 on the horizontal axis and data of the per capita income on the vertical axis. The vehicle data are provided by the Bangladesh Road Transport Authority (BRTA) Website. However, the data from 2020 is not taken because it is not representative of the typical trend due to the pandemic.In Figure 1, public transport formed a rough Kuznets curve along the per capita income until 2018. Still, the number increased slightly in 2019, emphasising government investment in the sector. However, in Figure 2, there is a different scenario. Private vehicles failed to establish a Kuznets curve along the per capita income. Over the years, the number of private vehicles tended to rise as the per capita income rose in the country and eventually plateaued in 2018 and 2019. So, even though public vehicles and per capita income form a Kuznets curve, it’s not the case for private vehicles.WHAT THE FINDINGS TELL US: The per capita income (as imperfect as it may be) gives a glimpse of the economic prosperity of the people in the country. With the increase in per capita income and economic development, there was initially an upward trend in the number of public vehicles on the roads. Still, with further economic prosperity, the number fell. The reason why it fell is reflected in Figure 2. As income increases, people tend to spend that money on luxuries; in this case, it is private transportation. That is the key reason why the number of private vehicles is increasing. Moreover, another reason for the upward trend in the number of private vehicles is that the country’s public transportation condition is substantially poor from a global standpoint. Traveling in public transportation is time-consuming and largely inconvenient due to delays. This remains a key reason why many commuters consider private transport a substitute for public ones, especially bikes. In recent times, there has been a substantial increase in bike sales; bikes are substituted for public transport. People can expect to see this upward trend in private vehicles in the future if the public transport sector is underfunded and lacks reform.The Kuznets analysis gives us a glimpse of comparing public and private transportation. This helps to understand the economics of transportation and how it influences people’s decisions in availing private and public transportation, as the findings expound on the rationale of people substituting public transport by private ones.

Syed Sabiq Ashraf and Nafisa Mesbah are students, Department of Economics and Social Science, Brac [email protected]@g.bracu.ac.bd

8:32am: Kingfisher’s French woes makes “sorry reading” Kingfisher is down 5.7% after its profit warning today. Richard Hunter, head of markets at…

The Inflation Impact on American Living Standards Since January 2021, American families have faced an uphill financial battle, needing an extra $11,434 each year to …

Shrugging off higher interest rates, America’s consumers spent enough to help drive the economy to a brisk 5.2% annual pace from July through September, the government said in an upgrade

US third-quarter economic growth revised up to 5.2%

The U.S. economy grew faster than initially thought in the third quarter, but momentum appears to have since waned as higher borrowing costs curb hiring and spending.

BDC says 45% per cent of Canadian entrepreneurs experienced mental health challenges in early 2023, but many are now seeking help. Read on.

The US economy grew 5.2 per cent in the September quarter, the fastest quarterly rate in nearly two years, beating expectations. Follow the latest updates in our live blog.

It is a pleasure to join you this morning in Salt Lake City for the Utah Banker and Business Leader Breakfast. 1 I find great value in engaging with and l

Sri Lankan aviation stands at a pivotal moment as it considers the transformation of Hingurakgoda Airport, also known as Minneriya Airport, from a primarily Air Force facility to a fully-fledged international….

/PRNewswire/ — A precise 2024 economic outlook would be invaluable, given such an evaluation is complex. While a recession is becoming less likely, many…

“China’s economy is in a property-led and fertility-led depression,” Yardeni wrote, adding that this “benefits countries that import Chinese goods at depressed prices.”

/PRNewswire/ — In the presence of His Highness Sheikh Khaled bin Mohamed bin Zayed Al Nahyan, the Crown Prince of Abu Dhabi, Abu Dhabi Finance Week (ADFW)…

Rose Paul has earned her share of praise and awards serving as the CEO of Bayside Development Corporation, the business arm of Paqtnkek Mi’kmaw Nation in Nova Scotia.

Shares are mixed in Asia after Wall Street benchmarks edged lower as investors looked ahead to updates on inflation and how American consumers are feeling about the economy

. Argentina’s recent presidential election saw the victory of Javier Milei, whose unconventional and worrying views, such as his opposition to abortion and ambivalent attitude towards the military government, have drawn attention. His economic proposals, such as replacing the peso with the dollar and eliminating the Central Bank, have also been debated. Dollarisation can act as a solution to hyperinflation, incentivising the economy to focus on export successes and easing conditions for foreign capital. Experiences of some countries, such as Ecuador, hold out promise for the project of dollarisation, with the economy showing considerable progress since 2000. However, the adoption of an external currency without the ability to chart independent policy can be seen in the case of Greece, where crushing austerity was adopted in exchange for financial assistance. Dollarisation is not a silver bullet, but if used well in conjunction with nimble domestic policy, can offer a route to success.

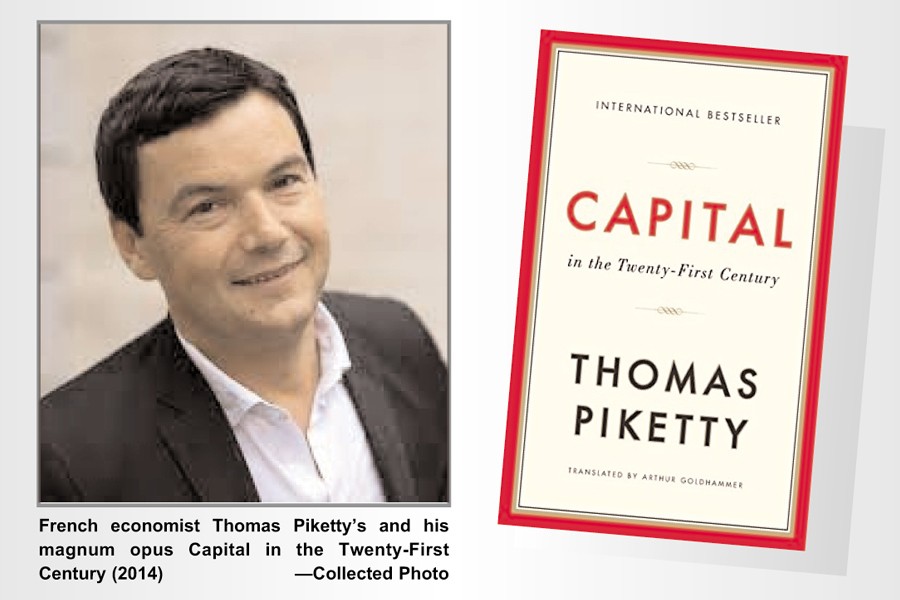

Thomas Piketty’s Capital in the Twenty-First Century (2014) has been a runaway best seller to the surprise of many. Over three million copies were sold as of 2022 and the curve is rising. Not since John Maynard Keynes’s General Theory of Employment, Interest and Money has a book on economics sold so many copies worldwide. It has stimulated, even provoked, historical, sociological and political science discussions despite being a book on economics. The sequel to the Piketty’s book, A Brief History of Equality (2021) heightened the interest on the main theme of the earlier book viz. inequality.The reception to the book, Capital in the Twenty-First Century, differed between the practitioners and academicians of economics and those outside of economics when the book first appeared. The first reason for the lukewarm interest shown to the book by the former is the European credentials of the author. Economic discipline having been the dominion of British and American economists for long. The second reason is the general impression among economists that a book written on empirical evidence lacks the rigour and elegance of one with theoretical underpinning. In respect of the first, nothing more than built-in bias among the majority of practitioners of economics can be cited as an intellectual lapse or wilful neglect. But the second, the lack of theoretical origin or grounding in Piketty’s analysis has been debunked by economists like Paul Kruggman who, in After Piketty (2019), wrote: “Piketty does not just offer invaluable documentation of what is happening, with unmatched historical depth. He also offers what amounts to a unified field theory of inequality, one that integrates economic growth, the distribution of income between capital and labour and the distribution of wealth and income among individuals into a single frame.” Robert Sollow, an elder statesman in economics of growth and a theoretician per excellence, thinks Piketty’s main point that as long as the rate of return on capital exceeds the rate of growth, the income and wealth of the rich will grow faster than the typical income from work, is a new and powerful ‘theoretical contribution to an old topic. ( in After Piketty, 2019).Leaving aside the issue of the pedagogical nature of Piketty’s best seller, his main findings may be revisited to find out the policy implications of his monumental work (both in timeline and physical volume). The title of the book will be abbreviated into Capital in the following sections.Findings of the book: Based on 15 years of research, Capital is devoted essentially to an understanding of the historical dynamics of wealth and income in France, Germany, England and America, since eighteenth century to the present. The sources on which the book has drawn are more extensive than any previous book on the subject.Piketty, after reviewing the growth trends and distributional patterns in industrially developed countries of global north concludes that the post-World War Social Democratic Age (1945-1980) were distinctly egalitarian places. In these countries, relative income differences were moderated as a result of which long- standing gaps in wealth, income, and employment were narrowed. This was accompanied by wide dispersal of political power in their populations. The claims of wealth to drive political directions and shape economic structures were kept within bounds, though not neutralised. But Piketty finds the Social Democratic Age as an unstable historical anomaly. He saw the rise of social welfare state as the consequence of declining power of the plutocratic elite. He traces declining post-tax inequality to the wars and the introduction of progressive taxation. This was not the same as the social insurance, labour productivity rise and welfare measures introduced in the late nineteenth and early twentieth centuries, because capital destroying wars, as well as periods of low inequality, were historical aberrations. He further observes that the Social Democratic Age was preceded by the First Gilded Age in Europe and America. In that preceding epoch the claims of wealth, especially inherited wealth, to drive political directions and economic structures were dominant. In that age, differentials in relative income and relative wealth were at extreme values. Piketty then proceeds to argue that the twenty first century is in an era of transition. While wealth concentration has just returned to its early twentieth century peak, it remains the case that for the top one per cent, the majority of income derives from earnings from labour, not from capital. On the other hand, inequality in capital income has been rising rapidly since 2000, whereas inequality in labour income has stayed relatively constant since then. Piketty observes sardonically that ‘’it has not yet transpired that ‘the past, devours the future’ but we are getting there’’.Piketty’s final conclusion is that due to the powerful forces generated by the underlying dynamics of wealth, it is most likely that the economies of the industrially developed countries are being driven to a Second Gilded Age in which once again the claims of wealth, especially inherited wealth, to drive political directions and shape political structures will be dominant, and in which differences in relative incomes, and even more, in relative wealth will once again be at extreme values.Piketty’s arguments: The central argument for the above conclusions or observations can be analysed in several steps.(1) A society’s wealth-to-annual income ratio will grow or shrink, to a level equal to its net savings and accumulation rate divided by its growth rate. (2) Time and chance inevitably lead to the concentration of wealth in the hands of a relatively small group— ‘the rich’. A society with a high wealth-to-annual-income ratio will be a society with an extremely unequal distribution of income. (3) A society with an extremely unequal distribution of wealth will also have an extremely unequal distribution of income, for the wealthy will manipulate political economy in such a way as to keep rates of profit in substantial levels and so avoid what Keynes called ‘the euthanasia of the rentier’ arguments. (4) Society with an extremely unequal distribution of wealth and income will be one in which, over time, control over wealth falls to heirs and heiresses – an ‘heirostocracy’. (5) A society in which wealth, especially inherited wealth, is economically salient will be one in which the rich will have a high degree of economic, political and socio-cultural influence. (6) The twentieth century (a) saw a uniquely high degree of economic growth due to growth forces of the Second Industrial Revolution and due to successful convergence of the global north to the economic prosperity landscape marked by America; (b) the twentieth century saw wars, revolutions, and socialising and progressive tax-imposing political movements generating uniquely strong forces pushing down the rate of saving and accumulation; (c) this trend got underway in twenty-first century in which all of these forces are now ebbing away.(7) Although the global north is far from the limit yet – the process of (1) to (5) above is still at work, it is substantially more likely than not to work itself to completion. It will deliver societies unequal in a number of ways in a half-century or so.Critique of Piketty’s arguments: According to some critics, it is debatable whether the rise in wealth- to- annual income ratios is driven by the forces Piketty highlights in Capital. And much more debatable is whether the rise in income inequality is being driven by a rise in wealth inequality that is itself a consequence of the rise in economy-wide wealth-to-annual income ratios. These points are contestable and are being contested.Some critics seek to cast doubt on Piketty’s argument regarding accumulation of wealth leading to a rising wealth-to-annual income ratio taking up Keynes’s argument that points to a rate of profit falling faster than the wealth-to annual income ratio, (‘euthanasia of rentier’), creating a society with a high degree of wealth but a low degree of income inequality.Another group of critics have argued that creative destruction, a la Schumpeter, will break up or at least limit the power of cross-generational dynastic accumulations. They further argue, echoing Frederich von Hayek, that the ‘idle rich’ are a valuable cultural resource precisely because they are not bound by the cycle of earning, getting and spending on necessities, and so can take the long view of things.Still others hope for a new industrial revolution to create more low hanging fruit and faster growth, accompanied by another wave of creative destruction that will short circuit the concentration of wealth in the hands of the few.Finally, as Robert Solow has shown, Piketty defines capital in the narrow sense of wealth, ignoring its role as a factor of production. In the latter sense of the term, capital leads to a rise in income that benefits all factors of production, including labour, undermining the force of Piketty’s argument on the inherent power of capital.Is Piketty right: The moot point is, are the arguments of Capital regarding built-in bias of capital towards accumulation of wealth in the hands of the few (the one per cent) right or at least, the scenario essayed by Piketty is plausible enough to worry about?The answer, according to many economists, sociologists, political scientists and historians (all engaged with the issue of inequality in their respective disciplines), is ‘yes’. The consensus is that Piketty is spot on in maintaining that in the industrialised economies of global north, as far back as one can look, ownership of private wealth, with its power to influence political economy, has historically been highly concentrated. He is right about a typical country in global north having the ratio of total private wealth to total income at about six around 150 years ago; he is also right in maintaining that in the Age of Social Democracy, fifty years ago, its capital-income ratio was about three. And his argument leading to the forecast that on the basis of the rising wealth-to-annual income ratio, income inequality of similar, if not higher, magnitude is likely to prevail during next fifty years ( from 2016, the date of publication of Capital).Economists who think one should not worry about concentration of wealth and income inequality are not few. According to them inequality is, if anything, good. It is an engine of faster economic growth, incentivising both investors and labour. Economists like Piketty are barking at the wrong tree, they contend. What problem a country going through growth experiences is not inequality but poverty, it is pointed out. Having identified the problem thus, this group of economists observes that industrially developed countries are now much richer than six generations ago. Back then, during the First Gilded Age, levels of inequality caused not just poverty but dire poverty. Inequality was a serious problem then. Now, because the global north is much richer, the degree of inequality that caused dire poverty then does not cause dire poverty now.This is an old argument which can be traced back to Adam Smith. He argued in his Wealth of Nations (1776) that the average working class Briton in eighteenth century lived better than his predecessors. In a later book, he observed that the consumption of the rich was limited and thus most of what they spent was in fact a contribution to the welfare of the poor. There is no dearth of economists taking the opposite stand and expressing a different view. Granting that economic growth above bare Malthusian subsistence in eighteenth century Britain was impressive and making allowance for the fact that economic growth since then has been impressive, too, they will not fail to point out that there are important reasons to care not just about historical standard of poverty but about inequality and what is called poverty today. It is not hard to prove the causality between inequality to health and other social welfare indicators. Robust data have been compiled and collated by Nobel Laureate Angus Deaton and Anne Cash (Rising Morbidity and Mortality among Americans, 2015) in their research on the daily struggles and misery of those left out of America’s economic growth benefits. Similar research findings document that once, narrowing gaps in employment, health, and overall well-being have stopped closing, and in some cases have reopened. It has been argued by economists who decry inequality that it is significantly likely that higher inequality will slow growth by depriving the economically disadvantaged of resources to invest in themselves and their children. The most trenchant criticism against inequality is that a polity in which plutocrats deploy their resources to have a loud voice will be a society in which government sets about solving problems of plutocrats and not the majority.It is no coincidence that the Occupy Wall Street movement in America and the wave of populist movements surging in countries of global north occurred just before and after the publication of Piketty’s Capital. Similar conclusion can be drawn from the recent decision by OECD countries to impose a minimum 15 per cent tax on corporate income to prevent multi- national corporations from enjoying tax-free status in safe havens or preferential treatment by host countries. These are powerful evidence that the book has caught the zeitgeist and struck a very loud and resonant chord in contemporary minds. The change in popular attitudes and aspirations will influence, if it has not already done so, the course of mainstream economics to re-set priorities, shifting emphasis from growth to alleviation of inequality. Or at least equal emphasis on both. For this change, Piketty’s monumental work, Capital, can take some credit.

[email protected]

The shift challenges assumptions about long-term gas demand and could mean natural gas has a smaller role in the energy transition than posited by the biggest, listed energy majors.

Las Vegas locals say they lost income as Formula 1 took over the Las Vegas Strip for the 2023 Grand Prix.

UBS expects the U.S. Federal Reserve to cut interest rates by 275 basis points in 2024, almost four times the market consensus.

Market Questions is the FT’s guide to the week ahead

27 Nov 2023 – The Dow Jones Industrial Average rose on Friday, as the major averages notched a four-week winning streak.

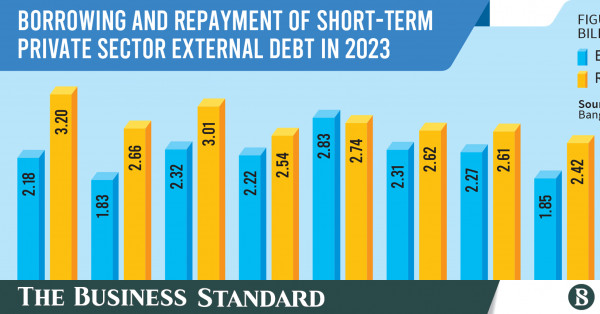

Inflow of short term external loans was $5 billion lower than the amount repaid in the first eight months of the current year, widening deficit in financial account

School at BRI-backed economic zone in Cambodia offers talents professional skills, language proficiency-

Uganda’s largest companies are allegedly abusing tax breaks

The University of the People, the first non-profit, tuition-fee-free, American, accredited online university, offers an innovative model to make quali…

Black Men Coalition of Dane County recently announced an exciting opportunity to spend a night with entertainment, food, and drinks at the Edgewater Hotel in downtown Madison at the non-profit organization’s first annual REVITALIZE Black Tie Fundraiser on Dec. 15.

Black Men Coalition (BMC) f

Updates on world markets and companies news

By Dr. Anthony Kellum The spending power of the Black dollar stands at a staggering $1.7 trillion, reflecting immense potential for community growth and economic empowerment. This financial strength, however, […]

London, United Kingdom, November 25, 2023 AppleAiBot, an innovative online financial platform, marks another successful year of empowering users globally. Since its inception, AppleAiBot has…

Rami Aboulnaga, Deputy Governor of the Central Bank of Egypt (CBE), said

Giant batteries that ensure stable power supply by offsetting intermittent renewable supplies are becoming cheap enough to make developers abandon scores of projects for gas-fired generation world-wide.

Global geopolitical tensions often play a very pivotal role in shaping people’s general perception of economic outlook. The current Israeli aggression against Gaza leading to more than 13,000 Palestinians death including over 5,500 children by the 3rd week of November is the latest chapter of a cycle of Israeli violence against Palestinians that has been going on in the occupied Palestine since Zionist colonial settler state Israel was created in 1948. Any rational debate or discussion on the topic of Palestine has become virtually impossible in the West because any support for the Palestinian cause or any criticism of the Israeli government or state faces charges of “antisemitism”. Given the US and its European allies’ support for the colonial settler state Israel and continuing Palestinian resistance against the occupation of their land, there seems no end of violence in sight in occupied Palestine. The policy of ignoring the historical context by the West has given rise to the current phase of the conflict. When the UN secretary general recently pointed out that the October 7 attack had a historical background, which is a demonstrably true statement, the Israeli Ambassador to the UN demanded that he be sacked immediately. In fact, the US and its European allies are partners in the occupation of Palestine. In the context of the current Israeli aggression against Gaza, US president Biden and his European partners like Sunak in the UK, Macron in France, Schotz in Germany, Meloni in Italy as well as Trudeau in Canada are fully implicated as accomplices of Netanyahu in mass murder.US president Joe Biden who famously said on June 5, 1986 that “If Israel did not exist, the United States would have to invent it”. He was a Senator at that time. His position now as the president of the US on Israel in the current phase of Israeli genocide against the Palestinians in Gaza has not changed, if anything it has further strengthened, he is even louder than before. In fact, from US president Harry Truman to Joe Biden that commitment has remained ironclad.The recent racist and Islamophobic rants in public against an Egyptian Muslim food cart vendor in New York and also calling the vendor a “terrorist” and saying the death of 4,000 Palestinian children in Gaza “wasn’t enough” by Stuart Seldowitz, a former deputy director of the US State Department’s Office of Israel and Palestinian Affairs (1999-2003) who worked for the National Security Council under the Obama administration following a State Department career that spanned five presidencies holding high positions indicate the type of people that are recruited to design and implement US government policies towards Arab and Muslim countries. During his tenure at the State Department, this unhinged outright racist was a three-time recipient of the Department’s “Superior Honour Award.The current Israel-Hamas war has the potential to cause immediate and long-term economic ramifications. The Russia-Ukraine conflict clearly demonstrated that how such conflicts can disrupt the very intricate interdependence that shape the global economic relations, notwithstanding the geopolitical implications. Many economists suggest that this war has the potential to disrupt global economy. Many central bank chiefs in the West believe that inflation will remain their biggest challenge for the next two years. Furthermore, uncertainty surrounding financial markets and the entire global financial system amid ongoing inflation, rising interest rates and ballooning government debt, the escalation of Israel-Hamas war, if militias in Lebanon and Syria join Hamas, could set off a major economic crisis. Such conflicts also often have a significant effect on stock markets, exchange rates and commodity prices. According to Goldman Sachs the Israel-Hamas war could have a significant economic impact. The longer term economic impact is more complicated to assess but such events can have negative impact on investors behaviour. However, all these potential effects depend on how the war develops in the coming weeks or months notwithstanding the ongoing Russia-Ukraine conflict which has already exacerbated the inflationary pressure.Bloomberg Economics has examined the likely impact of the war on the global economy under three alternative scenarios. In all three cases, while the magnitude will be different but the direction is the same – more expensive oil, higher inflation and slower growth. It estimates oil prices could soar to US$150.00 a barrel and global growth drop to 1.7 per cent and a recession that takes about US$1 trillion off global output.Oil is the most traded commodity in the global market. The oil market is especially a very volatile market because it is both a scarce and an essential commodity facing an inelastic demand. Any threat of disruption in oil supply now due to the Israel-Hamas war can cause oil prices to rise, usually described as the “oil price shock.” Such a shock would further push up food price inflation which has already been at an elevated level in many developing countries including Bangladesh. If the war were to escalate, not only developing countries but developed world would also face rising food and energy prices, thus intensifying food insecurity across the world.Oil prices have been volatile since Hamas launched its attack on Israel which Hamas named as Operation Al-Aqsa Flood (In Arabic ‘amaliyyat tufan al-’ Aqsa) on October 7. According to the latest World Bank’s quarterly update crude oil prices could rise to more than US$150.00 a barrel if the Israel-Hamas war escalates. But this is not surprising; conflicts in the Middle East tend to lead to spikes in oil prices as was seen during the 1973-74 oil embargo, the Iranian Revolution of 1978-79, the Iran-Iraq war of 1980 and the first Gulf war of 1990-91. In fact, since the war began, Brent crude oil and European natural gas prices went up by around 9 per cent and 34 per cent at the peak respectively.Already rising interest rates to fight inflation are intensifying financial pressures on businesses and households in the advanced as well as developing countries. Many businesses are considering laying off workers in the very near future to deal with the rising costs of doing business. Households are faced with rising grocery and energy bills denting consumer confidence. Usually during periods of war and other conflicts, general consumer confidence is the most important potential channel for spillover effects. The Eurozone area experiences a substantial deterioration in consumer confidence in the aftermath of the Russia-Ukraine conflict. The Israel-Hamas war has caused elevated levels of uncertainty both within the region and around the world with implications for consumer confidence.Meanwhile, it has been confirmed that Israel and Hamas have approved a ceasefire deal and hostage swap amid the unfolding genocide in Gaza mediated by the Qatari government. The deal was announced on last Wednesday (November 22). But Israeli prime minister Netanyahu declared that his country would continue the war until the elimination of Hamas was complete. It now appears that the deal is already stalling.But Gaza has already suffered massive destruction of houses, basic infrastructures, educational and health facilities including death of about 13,000 Palestinians including over 5,500 children. In fact, Israel’s land, sea and air assault on the Gaza Strip, triggered by Hamas’s cross-border attack on Israel on October 7, has brought upheaval and destruction to Gaza on a scale never seen before in the enclave.In fact, on November 13, Israel’s agriculture minister Avi Dichter described his country’s bombing of Gaza with a very concise phrase “Gaza Nakba 2023:That’s how it’ll will end.” This is worthy of an operational name for planned genocide and very symptomatic of the country’s descent into the abyss.By the time ceasefire was agreed by Israel and Hamas, 13,000 Palestinians were killed, 51.4 percent of all Gaza housing units had been destroyed. Although Gaza has a long history of conflict, there are no parallels to the scale of the present devastation. It is estimated that the economic cost of Israel’s ground operation in Gaza in 2014 was more than $6 billion. The current war is already longer and far more destructive. The war will push hundreds and thousands of Palestinians into poverty.According to Bloomberg, Israel’s aggression against Gaza has cost the Israeli economy close to US$8 billion by the middle of November with a further US$260 million in losses incurred with every passing day. According to the Times of Israel (November 21) the war is costing US$269 million a day. The total cost of war is estimated to amount to around 10 per cent of Israel’s GDP. The credit rating agency Moody’s is currently considering downgrading the Israeli government’s A1 credit rating.The Financial Times in an investigative report published on November 6 provided the devastating toll of Israel’s war of aggression against Gaza and how it is impacting on businesses, employment, consumer finance and the Israeli government itself. The Israeli army summoned 360,000 additional reservists, around 8 per cent of Israel’s work force for the war on Gaza to add to its active military force of 150,000. Since military service is compulsory for Israelis aged between 18 and 40, thousands of workers are leaving their usual jobs to join the front line.The India-Middle East-Europe-Economic Corridor (IMEC) was announced on the sidelines of the G20 meeting in New Delhi on September 9, 2023. The corridor was proposed from India to Europe through the United Arab Emirates, Saudi Arabia, Jordan, Israel and Greece. This is the latest in a series of initiatives led by the United States aimed at countering China’s Belt and Road Initiative (BRI) and to isolate Iran but more importantly to foster a close economic link between the major Arab economies and Israel. Now the IMEC has become a casualty of Israel’s war on the Palestinians in Gaza. However, it is to be noted that the IMEC faced many serious challenges even before the Israeli aggression against Gaza.Hamas’ attack on October 7 achieved significant successes challenging established security measures and potentially signalling the beginning of a larger unravelling of the Zionist Project. Risks for Israel have never been higher. The 7th October attack punched a big hole in Israeli national confidence; yet the Zionist settler colonial state still remains seriously deluded about its economic and military prowess. Israeli prime minister Netanyahu declared to eliminate Hamas and its rule in Gaza, but despite heavy aerial bombardments and the massive ground offensive, these objectives are far from being achieved. Let me conclude by quoting Fyodor Lukyanov, the Chairman of the Presidium of the Council on Foreign and Defence Policy in Russia “the Palestinian question has been the quintessence of 20th century international politics. We are probably witnessing the end of this today, in the sense of policy and what it has yielded.”

[email protected]

Xinhua Headlines: Xinjiang land ports play robust role amid efforts to expand opening up-

Professor Peter Diamond, a Nobel laureate in economics, stated in his presidential address at the 2004 meeting of the American Economic Association that “many young economists and economics students say that they expect to get no benefits at all from Social Security. This expectation does not seem sensible to me.” He further stated the trust […]

Financial literacy education is key to protecting Indians from scams in era of superfast payments

Seven possible explanations for what’s going on

Pakistan’s economic crisis is as much a political as it is an economic challenge.

Manufacturing PMI falls for fifth month as Beijing prepares to unveil growth target at annual parliament session

Finance expert Dr. Jeff Jones offers insights on managing personal finances better.